Cashless ATMs vs. Reverse ATMs: Understanding the Differences, Benefits, and Risks

July 14, 2026

By Wade Zirkle, CEO of BluePoint ATM Solutions

Although they are sometimes confused, Cashless ATMs and Reverse ATMs (also known as Cash-to-Card Kiosks or Prepaid Kiosks) have very different use cases. A cashless ATM enables consumers to access purchasing power from their bank account without dispensing cash, while a Reverse ATM converts physical currency into digital spending power through a prepaid card.

Both technologies are designed to facilitate cashless transactions, but they differ dramatically in their operation, customer experience, regulatory framework, and risk profile.

What Is a Cashless ATM?

Despite its name, a cashless ATM is neither an ATM nor is it Cashless.

Instead, the customer inserts or taps a debit card into a countertop device, enters a PIN, and authorizes a transaction over a PIN debit network. Rather than a machine dispensing the currency, the customer receives the cash manually, over-the-counter, from the clerk, which gives the customer cash purchasing capability. Cashless ATMs have historically been used in cannabis dispensaries, where federal law prohibits traditional POS transaction processing.

What Is a Reverse ATM?

A Reverse ATM converts physical cash into a prepaid card that can be used anywhere Visa/Mastercard prepaid cards are accepted.

These systems are increasingly found in:

- Stadiums/Arenas

- Universities

- Theme parks / Attractions

- Airports / Transit Hubs

- Hotels

- Locations that do not accept cash

How a Cashless ATM Works

- Customer inserts a debit card.

- Customer enters a PIN.

- Funds are verified.

- A PIN debit transaction is authorized.

- The clerk hands the cash to the customer, who then has cash for their purchase.

How a Reverse ATM or Cash-to-Card Kiosk Works

- Customer inserts cash.

- Currency is counted and verified.

- Value is loaded onto a prepaid card which is dispensed instantly.

- The card can be used for purchases.

- No bank account or PIN is required.

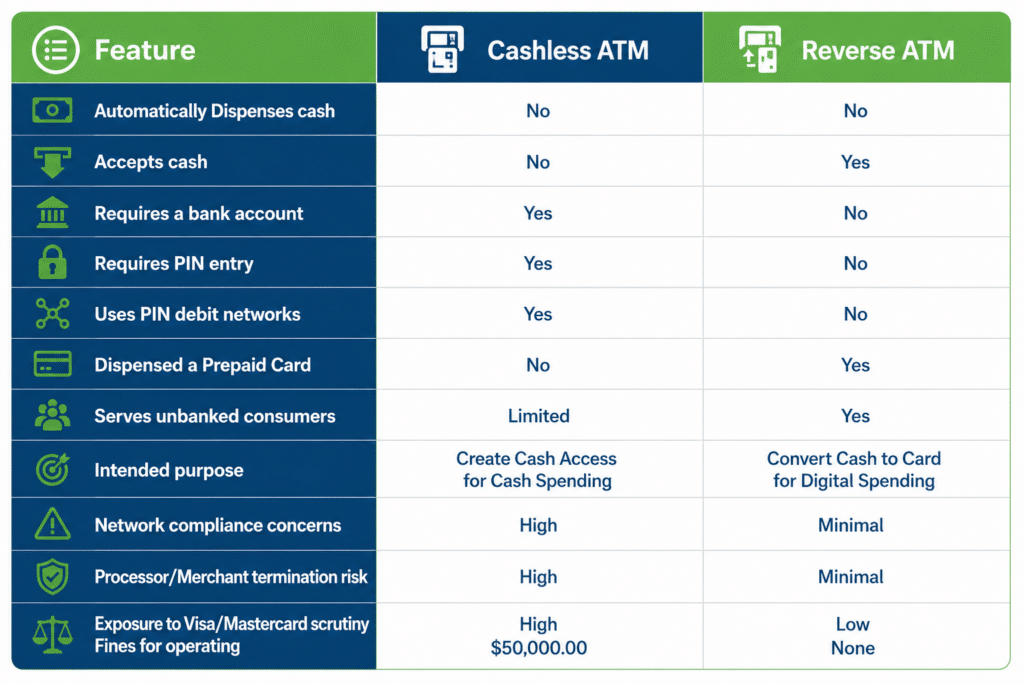

Side-by-Side Comparison

Advantages of Cashless ATMs

Cashless ATM systems may provide:

- Faster cash sales

- Reduced after hours physical theft exposure

- Reduced armored carrier expenses

- Improved customer convenience

Advantages of Reverse ATMs

Reverse ATMs provide several advantages:

- Inclusion of cash-paying customers

- Support for unbanked consumers

- Reduced / Eliminated cash acceptance at the register

- Faster checkouts

- Enhanced security

- Lower cash management costs

Because they operate through established prepaid card frameworks, they are widely used in fully cashless environments.

Cash-to-Card Kiosks enable organizations to go cashless without excluding customers who prefer or rely upon cash.

By converting cash into digital spending power, they bridge the gap between cash users and cashless merchants.

The Compliance Difference

One of the largest distinctions between these technologies involves network compliance.

Cashless ATMs have attracted scrutiny because transactions resemble retail purchases while being processed in a manner similar to ATM withdrawals.

By contrast, Reverse ATMs operate through established prepaid card programs and generally fit squarely within existing payment frameworks.

Similarly, Prepaid Kiosks are designed around recognized stored-value products and face little controversy.

Visa and Mastercard Concerns

Visa and Mastercard have repeatedly stated that an ATM, by definition, dispenses cash via an automated mechanism (not a human).

Cashless ATMs have been criticized because they may present a retail purchase as though it were an ATM withdrawal.

Card networks have expressed concerns regarding:

- Transaction transparency

- Merchant category accuracy

- Consumer disclosures

- Network integrity

As a result, many banks, processors and merchants have become increasingly cautious regarding these devices.

Risks of Operating a Cashless ATM

Businesses considering a cashless ATM program should understand the potential risks.

Processor Termination

Merchant accounts may be terminated if processors determine that the activity violates network rules.

Loss of Bank Sponsorship

Acquiring banks may discontinue support.

Frozen Funds

Processors may delay settlements or hold reserves.

MATCH List Placement

Future payment processing relationships may become more difficult to obtain.

Contractual Liability

Merchants may ultimately bear assessments and penalties imposed on processors or acquiring banks.

Regulatory Scrutiny

Cashless ATMs are attracting increasing scrutiny from networks and regulators. Merchants may have their accounts permanently shut down.

Financial Penalties

Visa / Mastercard issues fines up to $50,000 per location, per violation.

Why Prepaid Kiosks Carry Lower Compliance Risk

Prepaid Kiosks and Reverse ATMs operate within established prepaid card frameworks, compliant with Visa / Mastercard network rules.

Consequently, operators generally experience:

- 100% compliance solution

- Minimal network controversy

- Strong processor support

- Long-term sustainability

Which Solution Is Better?

Cashless ATMs May Appeal When:

- Customers primarily use debit cards and must pay with cash.

- PIN Debit transactions are more efficient to serve customers.

- Fast check-outs are important.

However, operators should carefully evaluate the legal, contractual, and network implications before deployment.

Reverse ATMs Are Best When:

- Venues are cashless.

- Cash-paying customers must be accommodated.

- Unbanked consumers are common.

- Compliance is critical.

- Organizations want to eliminate cash acceptance.

- Customer inclusion is essential.

- Long-term network stability is a priority.

- Minimal compliance risk is desired.

Conclusion

Although they are often grouped together, Cashless ATMs and Reverse ATMs are fundamentally different technologies.

Cashless ATMs convert bank-account funds into purchasing power but may expose merchants to increased processor, contractual, and network risk. Reverse ATMs (a.k.a. Cash-to-Card Kiosks or Prepaid Kiosks) convert cash into digital spending power through established prepaid card programs and generally operate within well-understood payment frameworks.

For merchants, the decision extends beyond convenience and operating costs. It also involves evaluating compliance risk, processor relationships, and long-term sustainability. Ultimately, both technologies provide access to purchasing power—but they do so in very different ways and with very different risk profiles.